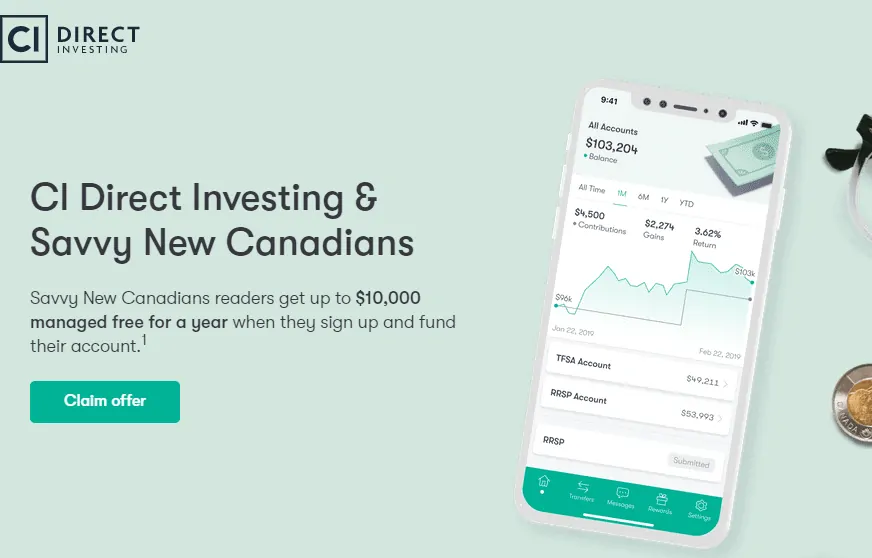

CI Direct Investing (formerly WealthBar) was the first full-service robo-advisor to set up a shop in Canada. While the online portfolio management industry is booming and has seen several fin-tech entrants in the last few years, CI Direct Investing can boast about its pioneering role in bringing low-fee wealth management to Canadians.

It used to be that the average investor could not access professional investment advice and certain financial asset classes if their net worth was not in the several hundreds of thousands to millions of dollars. And although mutual funds have been easily accessible, they come with a high price tag (Management Expense Ratio – MER).

Given these alternatives, if you did not have the confidence or know-how to DIY your investing through the use of a self-directed brokerage account, you were usually stuck with high-fee low-performing mutual funds.

What robo-advisors do is simplify your investing and make wealth-building accessible to everyone, irrespective of their financial status. Like the folks at CI Direct Investing often like to point out, they have made “Wall Street investing (possible) for Main Street Canadians.”

This CI Direct Investing review covers the investment options they offer everyday Canadians, unlimited financial advice, fees, portfolio types, performance, and more.

About CI Direct Investing (WealthBar)

CI Direct Investing is one of Canada’s online portfolio management advisors. It was founded in 2013 by Tea and Chris Nicola.

At CI Direct Investing, investors receive financial advice and are provided with custom low-cost ETF portfolios that meet their investing needs and are maintenance-free.

CI Financial Corp. (CI) acquired a 100% stake in WealthBar in 2020. The company manages approximately C$166 billion in assets.

CI Direct Investing Accounts

CI Direct Investing (formerly WealthBar) offers Canadians access to the following investment accounts:

- RRSP – Individual, Spousal, and Group

- RESP

- TFSA

- RRIF

- LIRA

- LIF

- Non-registered investment accounts (Individual and Joint)

- Corporate/Business investment accounts

How To Open a CI Direct Investing Account

Opening a new account is a breeze and should take no more than 15-20 minutes.

Step 1: Visit CI Direct Investing.

Step 2: Select the account type you want to open (TFSA, RRSP, RESP, etc.). Answer a few questions they use to determine your risk tolerance and investment objectives and provide you with a recommended portfolio. You will also be required to enter your basic personal details.

Step 3: Fund your account so your portfolio manager can invest it on your behalf. You are now on your way to building wealth!

If you move your investments from another institution to CI Direct Investing, they will refund any transfer fees you pay (up to $150) if your portfolio is more than $25,000. The minimum investment amount is $1,000.

Some of the information you should have on hand to speed up your account-opening process include:

- Your social insurance number

- Banking account information

- Employment details

- Investment and debt balances

CI Direct Investing Portfolios

CI Direct Investing offers low-cost portfolios that are designed to fit individual investors. Based on your risk tolerance and investment objectives, your recommended portfolio is one of the following:

- Safety ETF Portfolio

- Conservative ETF Portfolio

- Balanced ETF Portfolio

- Growth ETF Portfolio

- Aggressive ETF Portfolio

Each of these portfolios is comprised of 8-10 individual low-cost ETFs from popular providers like Vanguard, iShares, Horizon, BMO, and Purpose, and includes:

- BMO Covered Call DJIA Hedged to CAD ETF (ZWA)

- Purpose High-Interest Savings ETF (PSA)

- BMO Equal Weight REITs ETF (ZRE)

- BMO Laddered Preferred Share ETF (ZPR)

- BMO High Yld US Corp Bd Hdgd to CAD ETF (ZHY)

- iShares Core MSCI EAFE IMI ETF (XEF)

- Vanguard Canadian Short-Term Corp Bd ETF (VSC)

- Horizons S&P 500 ETF (HXS)

- Horizons S&P/TSX 60 ETF (HXT)

- Invesco Cleantech ETF (PZD)

Why Choose CI Direct Investing For Your Investing?

1. Customized Financial Advice: When you open an account, you get a dedicated financial adviser who is available to answer any questions you may have.

2. Diversified Portfolio: Your customized portfolio is built with diversification, risk reduction, and returns maximization in mind.

3. Financial Planning: You can create a financial plan(s) using the financial planning tool available on your dashboard. This versatile tool can show you your current financial situation vs. the various scenarios that can get you to your financial or retirement goals.

For example, how much will you need to invest in your RRSP, and how long will your savings last in retirement? A licensed financial planner is available to go through the plan with you.

4. Simple Fees: Investing fees can become complicated, particularly when you have all kinds of embedded fees or commissions that are not apparent upfront. At CI Direct Investing, the pricing is simple – no commissions are earned on ETFs, and there are no trading fees.

5. Automatic Rebalancing: Your portfolio is automatically rebalanced if it deviates more than 2.5% from the target allocation.

6. Socially Responsible Investing (SRI): They offer you an opportunity to invest in ways that align with your beliefs and which are beneficial to the environment using the First Trust Clean Edge Green Energy ETF [QCLN].

7. Security: Your money is held with an independent custodian (NBIN, CI Investor Services, and Qtrade Credential Securities), who are members of IIROC and CIPF. If these custodians go bankrupt for any reason, your funds are insured for up to $1 million per account category.

Other benefits of investing with CI Direct Investing include:

- Estate Planning

- Tax Optimization

- Insurance Needs Analysis

- Investment Assessment

- Corporate Tax Planning

- Mobile-friendly app for tablets and smartphones

- Available to Quebec residents (RESPs)

- Investing options for Canadians living abroad

CI Direct Investing Fees

Robo-advisors are popular mostly because they help the average investor save on investment fees. While the average annual MER charged by mutual funds is around 2.20%, robo-advisors charge much less for managing your money.

CI Direct Investing has a tiered fee system that ranges from 0.35% to 0.60% of your assets per year. This fee covers all the services you get, including portfolio management, trading charges, re-balancing, financial advice, and more.

Sample Fees

| Investment | CI Direct Mgt. Fee/ month | Mutual Fund Fee/ month |

| $5,000 | $2.50 | $9.17 |

| $10,000 | $5.00 | $18.33 |

| $25,000 | $12.50 | $45.83 |

| $50,000 | $25.00 | $91.67 |

| $150,000 | $75.00 | $275 |

| $500,000 | $191.67 | $916.67 |

In addition to the annual management fee (0.35% to 0.60%), you will also pay ETF MER fees that are built-in and paid to the ETF companies directly. This fee ranges from 0.19% to 0.26%. ETF fees normally apply even if you buy the ETF yourself using your online brokerage account.

CI Direct Investing (WealthBar) vs. Wealthsimple Fees

CI Direct Investing and Wealthsimple differ in their pricing structure in that while CI Direct Investing’s fee schedule is multi-tiered, Wealthsimple has two fixed rates: 0.50% for accounts under $100k and 0.40% for portfolios exceeding $100K.

Let’s look at a few scenarios:

Scenario 1: If you have a modest portfolio with $20,000. Your annual fee is:

- CI Direct Investing: $120/year

- Wealthsimple: $100/year

- Typical Bank Mutual Fund: $440/year*

Scenario 2: If you have a modest portfolio with $100,001. Your annual fee is:

- CI Direct Investing: $600/year

- Wealthsimple: $400/year

- Typical Bank Mutual Fund: $2,200/year

Scenario 3: If you have a modest portfolio with $500,000. Your annual fee is:

- CI Direct Investing: $2,300/year

- Wealthsimple: $2,000/year

- Typical Bank Mutual Fund: $11,000/year

*Using an average mutual fund fee of 2.20%

As you can see, both Wealthsimple and CI Direct Investing can literally save you hundreds of thousands of dollars over a lifetime compared to many of the mutual funds sold by your bank.

As your account grows, you save a bit more on management fees with Wealthsimple. However, note that when choosing between robo-advisors, you should be taking more than just fees into consideration.

Wealthsimple Invest

Professionally managed ETF portfolios

Multiple account types

Auto rebalancing and div reinvesting

Get a $25 bonus with a $500 deposit

Is CI Direct Investing Safe?

When you invest with CI Direct Investing, your funds are protected up to $1,000,000 per account category. This is because your money is held by custodians who are members of the Canadian Investor Protection Fund (CIPF).

For the safety of your personal information, the company uses bank-level encryption to protect your information and funds.

CI Direct Investing Performance

If you are interested in the performance of CI Direct Investing portfolios over the years, you can check their website.

As always, please note that historical performance does not guarantee future results!

Is CI Direct Investing For You?

You do not have to be considered “high-net-worth” to invest like one. Robo-advisors like CI Direct Investing simplify the investing process for those who want a simple fix to take their wealth-building efforts to the next level.

If you do not want to pay high mutual fund fees and are not confident about going it alone using a self-directed brokerage account, robo-advisors are a great option.

They figure out your ideal portfolio, re-balance it for you, and provide financial advice… all at a comparatively low annual fee. Investing doesn’t get any easier than this!

CI Direct Investing Review 2022

-

Management Fees

-

Account Minimum

-

Investment options

-

Ease of Use

-

Customer Support

Overall

Summary

CI Direct Investing is one of Canada’s best robo-advisor platforms. This CI Direct Investing review covers its investment performance, portfolios, fees, and more. Learn about how to invest your first $10,000 free of charge.

If you had to compare WealthBar and Wealthsimple for their financial planning advice, how would they rate?

@Maria: I would say the same. In general, robo-advisors offer basic financial advice if you are on their “basic” investment account. If you plan to invest a bigger portfolio($100K+), the financial planning available increases.

Cheers!

You numbers are a bit off for the monthly fees. You pay .05% per year at WS. So $20,000 invested would be $100 in management fees for the YEAR not the month.

@Jason: The numbers quoted in the post are per year (annual). Or, maybe I’m missing something?

Do they offer a referral program for clients?

I like the direct comparison of the fees for each of Wealthbar, Wealthsimple, and mutual funds. It really shows how expensive mutual funds are.

I see that each of the 3 scenarios given in the comparison is described as a “modest portfolio”. Is that like a “balanced” portfolio? The term “modest” isn’t used anywhere else in the article.

We can’t decide between WealthSimple and CI Direct. We have 450K and care about ethical investing while maximizing returns, and do not want to be involved in the day-to-day thinking about topping up our RRSPs and TFSAs and making everything tax efficient. We plan to use quite a bit of that for a down-payment in a year or two and will want advice on how much to allocate to that down the road. We’re residents in Vancouver and one of us is a dual citizen with the US – we have a US bank account in addition to our Canadian but it currently has a limited amount in it.

Thoughts on which one to go with? Can you compare the ethical investing opportunities more specifically?

@Jack: I haven’t taken a close look at the SRI’s offered by both companies. I couldn’t find much online about CI’s Cleantech portfolios, however, you can read about Wealthsimple’s SRI’s in the link below:

https://www.wealthsimple.com/en-ca/magazine/sri-portfolio

If you plan on using part of the funds for a downpayment soon, you should probably be looking at keeping that part of the money in something more conservative, such as a GIC, HISA, or bond portfolio. You don’t want to risk having to liquidate your position when the market is down.