It doesn’t take long for many newcomers to Canada to get hit with the ugly reality that they need a good credit score to access competitive interest rates on credit products.

And to achieve the aforementioned, they must first build a credit history right here in Canada.

When I first arrived in Canada in 2011, I knew nothing about credit scores as my home country did not have a national credit reporting system at the time.

Because I was wary of taking on debt, it took a while for me to build a healthy credit history as I was avoiding the very things needed to do so.

Read on to learn about how to build your credit history and increase your credit score as a new immigrant in Canada.

Key Takeaways

- Getting a credit card and applying for a personal loan or line of credit are two of the best ways for new immigrants to build credit in Canada.

- To increase your credit score, pay bills on time, limit your credit usage, and don’t send out multiple credit applications at once.

- Some of the best credit cards you can use to build credit history in Canada include the Tangerine Money-Back Credit Card, KOHO Prepaid Mastercard (with credit builder add-on), and Neo Credit.

What is a Credit Score?

A credit score is a three-digit number that lenders (credit card companies, personal loan and mortgage providers, etc.) use to assess your creditworthiness.

This number ranges from 300 to 900 in Canada, and it tells potential lenders whether you have responsibly paid off your debts in the past.

The higher your credit score is, the better. A “good” to “excellent” credit score increases your chances of qualifying for the best (low) interest rates, which translates into more money in your pocket.

So, what makes a good credit score? It varies depending on who you ask.

As per Equifax, a credit score between 660 and 724 is considered good. Scores above this range fall in the “very good” to “excellent” categories.

Why Your Credit History Matters

Why is it important to build a credit history? To answer this, we must look at how your credit score is derived from your credit report.

Credit bureaus like TransUnion and Equifax routinely receive information from lenders and other financial institutions indicating when you paid your bills, missed a payment, obtained new credit, and your credit balances.

They compile this information over time into your credit report and then calculate your credit score using your credit report (and the information contained therein) and complex scoring algorithms.

Information from other sources (e.g. public records) may also factor into your credit score calculation.

It is not unusual to get different credit scores from Equifax and TransUnion, as their scoring models differ. Lenders may also have their own in-house credit scoring metric that may include other factors.

Without a credit history and report in Canada, there’s no way to calculate your credit score.

How To Build Credit as a New Immigrant in Canada

To build a credit history, you need to take on some form of debt (i.e. credit).

Below are some options:

1. Get a Credit Card

Using a credit card is one of the easiest ways to build credit in Canada as a newcomer.

When you use a credit card and pay off your balance, the credit card company shares this information with the credit bureaus, and it is included as part of your credit report.

That said, qualifying for a credit card may be challenging because… they want you to have a good credit score!

How do you build a credit history when you can’t even qualify for a credit product?

Thankfully, there are several options:

Unsecured credit card: Ideally, you want to apply for an unsecured credit card that does not require you to provide collateral, i.e. a security deposit.

Secured credit card: If your lack of credit history makes it harder to qualify for an unsecured credit card, apply for a secured card.

The main difference between secured vs. unsecured credit cards is that you need to provide collateral to get a secured card.

For example, you may qualify for a secured credit card with a $1,000 credit limit by depositing $1,000 in a Guaranteed Investment Certificate (GIC) account at the bank.

When you close your credit card account or after you have increased your credit score, they give you back the deposit.

If you default on paying back your card balance, the bank is protected as they can simply keep your deposit.

Both secured and unsecured cards report your transactions to the credit bureaus. Ask your bank if a secured credit card is an option if they decline your application for an unsecured card.

Store credit card: Credit cards issued as part of a retailer’s loyalty rewards program are often easier to qualify for, and they offer benefits similar to regular credit cards.

Examples of store credit cards include:

Student credit card: If you are an intentional student, you may qualify for an entry-level credit card designed with students (low income and credit score requirements) and newcomers in mind.

Some examples of student-friendly credit cards include:

Prepaid card: Prepaid cards generally work like gift or debit cards and won’t help you build a credit history. However, with the KOHO Prepaid Mastercard, you get many of the benefits of a cash back credit card and can also build your credit score.

You can qualify for KOHO with a temporary or student visa (no credit history needed). When you add the credit-building feature, they report your transactions to a credit bureau, helping you improve your credit score.

Newcomer bank programs: Some banks offer programs specifically designed to help newcomers integrate into Canada’s financial system.

These programs often include banking bundles with chequing, credit cards, international money transfers, savings, and personal loan accounts.

You may be able to qualify for an unsecured credit card to build your credit history in Canada.

Newcomer bank account programs include:

- RBC Newcomer Advantage

- Scotiabank StartRight Program

- HSBC Bank Canada Newcomers Program

- CIBC Welcome To Canada Banking Package

- Simplii Financial Newcomer Program

- TD New to Canada Banking Package

2. Apply for a Personal Loan or Line of Credit

It takes a while to build enough credit history that translates into a good or excellent credit score.

If you’d like to get an 800+ credit score at some point, you will need to have different types of credit.

I got a rude shock when at some point during my post-grad studies, I wanted to buy a car, and I couldn’t afford to pay everything in cash upfront.

I had approached my bank for a car loan, but they declined my application. The car dealership then offered me double-digit interest rates from their “alternative” lenders, and this was when the importance of building a credit history dawned on me.

As much as getting your first credit card will help get you started on your way to a good credit score, you may need to juice things up a bit if you plan to increase your credit score quickly.

Diversify your credit with a loan product or line of credit. This could mean applying for a small personal loan or car loan.

Even if you have the cash to pay for a car outright, it may make sense to finance a small portion of the cost and quickly pay off the loan within 6 months to 1 year.

This strategy limits your interest fees while helping you build a more diverse credit history.

Other things like financing your cell phone plan can also be beneficial for credit building.

How To Increase Your Credit Score

Getting a credit card, loan, or line of credit will help you build a credit history.

That said, to increase your credit score steadily over time, you will also need to deploy these strategies:

A. Pay bills on time: Pay your credit card bills or loan repayments on time. Missed payments negatively impact your credit rating, and the resulting fees and penalties push you further into debt. Automate bill payments when you can so you don’t forget.

B. Limit your credit usage: Do not max out your cards or line of credit. Keep your outstanding balance to no more than 35% of your limit at any point in time (i.e. credit utilization ratio). For example, if your credit card has a $5,000 limit, limit your usage to $1,750.

C. Limit credit applications: While you want to hold a mix of credit types, don’t send out multiple applications all at once. Each time a lender assesses your credit application, they may pull your credit report (i.e. hard inquiry), which can negatively affect your credit score.

If you are shopping for auto financing or personal loan rates, limit it to a 2-week window so that the multiple hard inquiries are combined into one, and the impact on your score is minimized.

Also, don’t just apply for credit just for the sake of applying.

D. Check your credit report for errors: Routinely monitor your credit report for errors. If you notice any errors, file a dispute with the credit bureau to remove them.

Common credit report errors include:

- Mistake in your personal information

- Payment history and account balance errors

- Negative information that has expired (e.g. bankruptcies or account collections).

Credit monitoring can also help you detect identity fraud early before lasting damage to your credit rating occurs.

The Financial Consumer Agency of Canada has more tips on improving your credit score.

How To Check Your Credit Score in Canada

You can check your credit score directly through the two main credit bureaus in Canada – Equifax and TransUnion.

Alternatively, you can also get your score for free through these financial technology companies:

Borrowell: Offers access to a free Equifax credit score that is updated weekly.

Loans Canada: Provides access to a free Equifax credit score that is updated regularly for free. Check it out.

Credit Karma: Offers access to a free TransUnion credit score that is updated monthly. Learn more here.

How To Check Your Credit Report in Canada

Like your credit score, you can access your credit report via the credit bureaus:

TransUnion: Referred to as a Consumer Disclosure. You can apply online or call 1-800-633-9980.

Equifax: Request your Equifax credit report by mail, in person, or by calling 1-800-465-7166.

If you sign up for weekly credit score updates through Borrowell, they also give you access to a free Equifax credit report.

Credit Cards To Build Credit History in Canada

There are many credit cards available in Canada that work well for newcomers. Below, I have listed a few no-fee card options you can try when getting started:

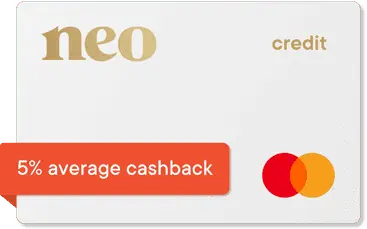

Neo Credit

Excellent credit card for cash back

Annual fee: $0

Rewards: Earn up to 15% cash back for first purchases at eligible partners, 5% average cash back at partner stores for subsequent purchases, and 0.5% cash back on average on all purchases.

Welcome offer: $25 bonus on approval.

Interest rates: 19.99% – 22.99% for purchases.

Minimum income requirement: None

Recommended credit score:

Fair

On Neo Financial’s website

The Neo Mastercard is one of Canada’s best cash back credit cards. Learn more about it in this review.

Tangerine Money-Back Credit Card

Best no-fee cash back credit card

Annual fee: $0

Rewards: Earn up to 2% unlimited cash back in up to 3 spending categories and 0.50% on all other purchases.

Welcome offer: Get an extra 10% cash back on up to $1,000 in spending in the first 2 months ($100 value).

Interest rates: 19.95% for purchases, balance transfers, and cash advances.

Minimum income requirement: $12,000

Recommended credit score:

Fair to Good

On Tangerine’s website

The 10% cash back offer applies when you spend up to $1,000 in the first two months. Learn more about the best Tangerine credit cards.

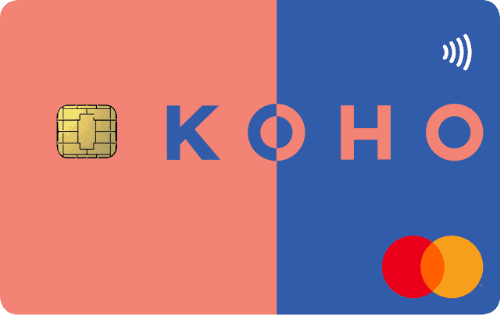

KOHO Prepaid Mastercard

Top prepaid card in Canada

Annual fee: $0* monthly for Essential card.

Rewards: Earn up to 5% unlimited cash back on debit purchases and earn 5% savings interest on your entire balance.

Welcome offer: $20 welcome bonus after your first purchase (use CASHBACK promo code when signing up).

Interest rates: 0%

Minimum income requirement: None

Recommended credit score:

None

On KOHO’s website

The KOHO Prepaid Mastercard is not a credit card. That said, when you subscribe to its Credit Building service for $7-$10 a month, they will help you build your credit score by reporting this payment to the credit bureaus.

Learn more in this KOHO review.

Simplii Financial Cash Back Visa Card

Excellent credit card for students and newcomers

Annual fee: $0

Rewards: Earn up to 4% cash back on high-spend categories.

Welcome offer: For your first 3 months, enjoy 20% cash back on eligible gas, groceries, drugstore purchases and pre-authorized payments (up to $500 spend).

Interest rates: 19.99% on purchases and 22.99% on cash advances.

Minimum income requirement: Minimum annual household income is $15,000.

Recommended credit score:

Good

On Simplii’s website

Learn more in this detailed Simplii Financial Cash Back Visa Card review.

For a secured credit card that can help you build or rebuild your credit, check out:

Other newcomer resources: