RBC is one of the biggest banks in Canada, and it has a variety of mortgage products to choose from.

Whether you’re buying your first home, a second property, or you want to refinance your mortgage, you should be able to find what you need.

In this review of RBC mortgages, I take a closer look at what’s on offer, list the main pros and cons, and compare other mortgage lenders to help you decide whether RBC is a good option.

Key Takeaways

- RBC is one of the Big 6 Canadian banks, providing a wide range of mortgage products.

- It offers several types of mortgages, including fixed and variable rates, with terms of up to 25 years.

- Due to its size, it is a trusted and reputable lender, and you may even be able to apply for a mortgage remotely.

RBC Mortgage Overview

RBC, or the Royal Bank of Canada, is one of the Big 6 banks. It was founded in 1864 and now has over 1,000 branches nationwide.

As you would expect, it offers many financial services, including mortgages.

Here you can find fixed-rate and variable-rate mortgages (open and closed), mortgages for first-time buyers, investment properties, HELOCs, mortgage refinancing, and more.

All the major options are available, plus an interesting Cash Back Mortgage for first-time homeowners and the RBC Homeline Plan, which combines a mortgage with a line of credit.

RBC Mortgage Rates

When you look for a mortgage, I recommend comparing the going rates from several lenders. These change constantly, so it depends on when you check them, but you can see all the latest RBC mortgage rates here.

RBC has fixed and variable mortgages, including both open and closed options. Fixed mortgages have terms from six months to 25 years.

Variable mortgages are available as a five-year closed or a five-year open mortgage.

I’d recommend checking for special offers. Again, these change regularly, but it’s always worth looking for special rates when applying.

Featured Mortgage Offer

Neo Mortgage

On Neo Financial’s website

- Compare mortgage rates across several lenders

- Access to competitive rates and online applications.

- Available Canada-wide

- Accepts a wide range of credit scores

RBC Mortgage Features

There are several features that, in my opinion, make RBC mortgages quite attractive.

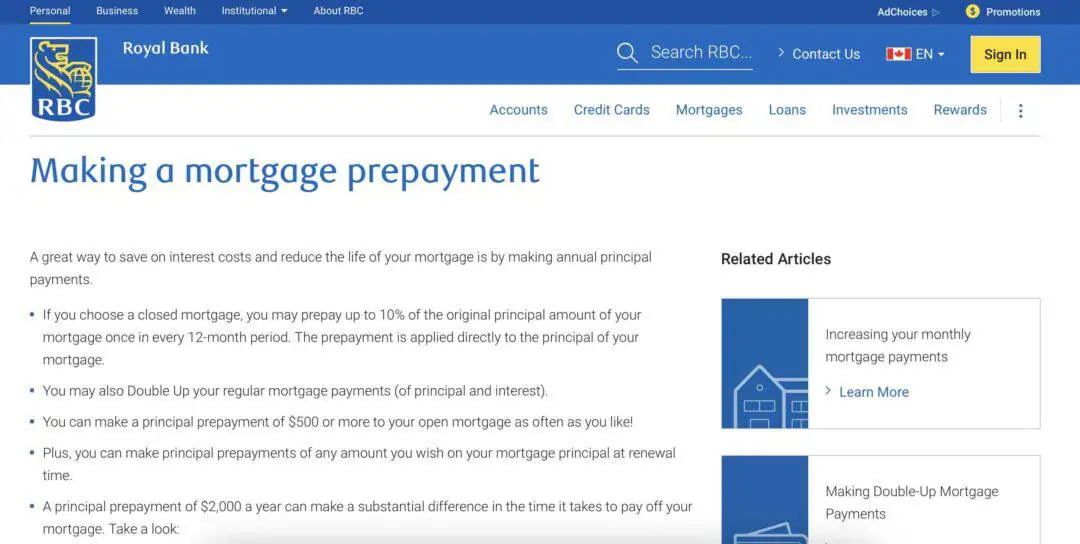

Prepayment Options

When it comes to prepayment options with a closed mortgage, you can prepay up to 10% of the principal every year. You can also double up your mortgage payments.

With an open mortgage, you can make a principal prepayment of $500 or more whenever you like.

Eligibility Requirements

The eligibility requirements are fairly standard.

You usually need a good credit score of 680 or more to apply, and your income will depend on how much you want to borrow.

A self-employed mortgage is also available, which is useful because it can often be a greater challenge for self-employed people to get a mortgage.

RBC also has several tools on the website to better understand how much you can qualify for, like the True House Affordability tool.

Mortgage Specialists

RBC has mortgage specialists available who you can talk to when you want to discuss your options and get help and advice.

Online Application

If electronic signatures are allowed where you live, you can send in the paperwork and complete the process remotely.

Get Pre-Approved

You can get pre-approved for a mortgage from RBC, and the rate will be held for 120 days.

RBC Homeline Plan

If you want to combine your mortgage with a HELOC, this is possible with the RBC Homeline Plan.

Cash Back Mortgage

New home buyers can get up to 7% of the mortgage value up to $20,000 with this special mortgage.

Pros and Cons of an RBC Mortgage

Pros

- Transparent with its rates, and you can quickly find them all on the website.

- Option to apply for a mortgage online.

- RBC will hold your rate for 120 days after you get pre-approved.

- Plenty of branches all over Canada.

- Good prepayment options if you want to pay off your mortgage faster.

- Large selection of mortgage products, including a Cash Back Mortgage.

- Wide range of mortgage terms up to 25 years.

Cons

- Only provides its own mortgage products, so you will have less choice than using a mortgage brokerage.

- It may not be a good option if you have a poor credit score.

How to Apply for an RBC Mortgage

To apply for a mortgage from RBC, contact one of their mortgage specialists to arrange a call, video chat, or meeting in person.

You may need to submit your documents in person, but you can complete the application remotely if electronic signatures are permitted in your province or territory.

Alternatively, you can request a pre-approval, which you can complete online.

To do this, gather all your documents, including proof of income, bank statements, Social Insurance Number, etc.

Fill out the pre-approval form online, and within 24 hours, you will be contacted by a mortgage specialist. They will ask more questions and collect any information they need.

If you get pre-approved, you will be given an interest rate that will be held for 120 days.

You can apply for full approval once you are ready to buy a property. This is not guaranteed, but there is a good chance you will be approved if your situation has not changed.

RBC Mortgage Alternatives

There are many mortgage providers in Canada. While RBC is a good option, it’s not the only place to look. Here are some of my recommendations to consider checking out.

Neo Mortgage

If you like the idea of applying for your mortgage remotely, Neo Mortgage might appeal to you.

This is a digital bank offering digital mortgages. You can get new mortgages here or renew or refinance your mortgage.

One of the major benefits is that you can complete the whole process from home, including signing legal documents.

However, Neo Mortgage does not provide its own mortgages. Instead, it checks the market for the best rates.

Nesto Mortgage

Nesto is a digital bank offering a fast, simple mortgage application process and competitive rates.

It provides mortgages for first-time buyers as well as refinancing and renewals. Again, it does not provide its own mortgages but scans the markets to find the best rates among partners.

BMO Mortgage

Another of the Big 6 banks in Canada, BMO offers similar products to RBC, including a line of credit, mortgage renewal, refinancing, etc.

However, it also holds your rate for 130 days following pre-approval, which is longer than most, and it has accelerated payment options.

Tangerine Mortgage

Tangerine is another digital bank that provides competitive rates for its mortgages. When you are pre-approved, it holds the rate for 120 days, which is the same as RBC. It also offers flexible prepayments.

It also offers mortgage refinancing, and applying for any of its mortgage products is quick and easy.

TD Mortgage

TD is another of the Big 6 Banks, and it offers similar mortgage services to RBC, including mortgage renewals and refinancing.

You can speak to mortgage specialists for advice and get pre-approved in as little as five minutes. Like RBC, it will also hold your rate for 120 days.

Is Getting an RBC Mortgage Worth It?

Should you get an RBC mortgage? That’s a decision you have to make. However, I’d recommend always comparing the options available at RBC and other mortgage providers like those I’ve listed above.

Try to find the best rate you can, but also a mortgage that suits your needs. You might want to at least get pre-approved if you are considering buying a property soon, and you are under no obligation to go ahead with it.

If you have other products with RBC, it could also be a good option.

There is nothing that makes RBC a bad option. It’s big, trustworthy, and transparent, and the online application option is a good feature.

Ultimately, it comes down to the current rates, how they compare with other providers when you apply, and whether it looks like a good fit for you.

FAQs

While RBC does not state a minimum credit score to get a mortgage, you will normally need a score of 680 or above.

It is very common for mortgage specialists to work on a commission basis, and this is also the case at RBC.

After you have been pre-approved for a mortgage, RBC will hold the rate for 120 days, which is in line with many other mortgage providers.

No one can say whether mortgage rates will go up or down in the next few months, so consider this when choosing a suitable mortgage for your needs.

Related: