Neo Financial and Tangerine Bank offer financial products and services to Canadians through their online platforms.

While Tangerine is a full-fledged online bank, Neo Financial is a financial technology company that is affiliated with banks like Concentra and ATB Financial.

This Neo vs. Tangerine comparison covers their product offerings, fees, pros, cons, and everything else you need to make an informed choice.

Neo vs. Tangerine

| Feature | Tangerine | Neo Financial |

| Ownership | Subsidiary of Scotiabank | Independent fintech partnered with Concentra Bank and ATB Financial |

| Account Types | Chequing, Savings (regular, TFSA, RRSP), Business, Investments, Mortgages, Credit Cards (two types), Loans | Hybrid, Savings (regular), Credit Cards (x2), Mortgages, Investments |

| Interest Rates | Competitive promo rates on savings accounts; up to 0.10% on chequing balance | High interest on savings accounts; 2.25% interest on hybrid account balance |

| ATM Access | Scotiabank ATMs in Canada, Global ATM Alliance abroad | Use of ATMs within the Exchange Network |

| Monthly Fees | No monthly fees for standard accounts; no annual fee for credit cards | No monthly fees for standard accounts; no annual fee for standard credit card (some paid options available) |

| Other Fees | Drafts, overdraft protection, NSF fee, paper statement, Non-bank ATM withdrawals, FX fee | Printed statements, over the limit, rush replacement card, and FX fee |

| Credit Cards | Tangerine Money-Back Credit Card and Tangerine World Mastercard | Neo Credit Card, Neo Secured Credit, Neo Money prepaid card |

| Mobile App | Yes, with robust features | Yes, modern and user-friendly |

| Customer Service | Phone, Chat, Email | Chat, Email, Phone |

| Security | CDIC eligible | CDIC eligible |

| Rewards Program | Cash back rewards | Cashback on Neo Credit Card, partner rewards |

| Credit Building | Credit products available for credit building | Neo Credit or Secured Card helps in credit building |

| Promotions | 10% cash back bonus on first $1000 credit spend ($100 value) | $25 bonus when approved for the credit card |

Below, I discuss each financial institution and how their financial services and products differ.

This includes a comparison of their chequing, savings, credit cards, investments, and borrowing products.

This guide also looks at their fees, promotions, security, and more.

What is Neo Financial?

Neo Financial is a fintech founded in 2019 by two SkipTheDishes co-founders, Andrew Chau and Jeff Adamson, and Kris Read.

It provides a variety of savings, spending, and rewards products and recently added mortgages and investments to the mix.

Learn more about the company in this Neo Financial review.

What is Tangerine Bank?

Tangerine Bank is the online banking arm of Scotiabank. It was formerly known as ING Direct when it was launched by The ING Group in 1997.

Tangerine Bank offers various financial products, including chequing, savings accounts, credit cards, Guaranteed Investment Certificates (GICs), investment funds, mortgages, and more.

Learn more about the company in this Tangerine review.

Neo Financial vs. Tangerine: Chequing Account

Neo Financial does not have a traditional chequing account. Its Neo Money account is a hybrid account with saving and spending features. I discuss this account in more detail under “savings.”

The Tangerine Chequing Account has no monthly account fees and offers:

- Unlimited debit transactions and Interac e-Transfers

- Access to 3,500 Scotiabank ABMs across Canada

- Mobile cheque deposits

- Tiered interest on your balance (0.01% to 0.10%)

- A debit card

Verdict: Tangerine Bank is a better choice if you only need a no-fee chequing account.

Neo Financial vs. Tangerine: Savings Accounts

Both financial institutions have an account that pays you interest on your deposits.

Neo’s “savings” account is called Neo Money, while Tangerine’s savings accounts include registered and non-registered versions.

Neo Financial: Neo Money

Neo Money is a hybrid account for saving, spending and earning interest on your money.

It pays a 2.25% interest rate on every dollar which is higher than what you will earn at some traditional banks.

While Neo Money is not a chequing account, it offers similar features, including free and unlimited Interac e-Transfers, deposits, and bill payments.

It also has no monthly fees and comes with a prepaid card you can use at ATMs.

You can manage your account using the Neo Financial mobile app and also link your bank accounts to other financial institutions.

Neo recently introduced a separate high interest savings account that pays a 4.00% interest rate.

Tangerine Bank: Savings Accounts

Tangerine Bank has several savings accounts, including general savings and:

- Tax-free savings account

- RSP savings account

- RIF savings account

- US Dollar savings account

The standard interest rate on its savings accounts is 0.70%, although new clients often get a higher promotional rate for a few months.

Verdict: The Neo HISA is better for higher non-promotional savings interest rates. That said, if you need a TFSA or RSP savings account that pays a competitive rate, you can check out EQ Bank.

Neo Financial vs. Tangerine: Credit Cards

Both Neo Financial and Tangerine offer rewards credit cards.

Read on to see how they compare.

Neo Financial: Credit Cards

Neo Financial offers two credit cards:

- Neo Mastercard (Neo Card)

- Neo Secured Credit Card

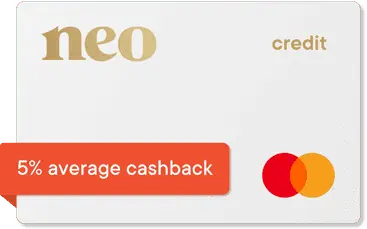

The standard Neo Mastercard has no annual fees and pays a 5% average cash back rate when you spend at participating retailers (Neo partners) and a minimum 1% cash back across all spending (subject to a limit of $5,000 spending per month).

Neo Credit card

Rewards: Average of 5% cash back at 12,000+ partners and a guaranteed minimum of 0.50% cash back across all purchases

Welcome offer: Get up to 15% cash back on your first-time purchases, plus a $25 welcome cash bonus.

Interest rates: 19.99% – 29.99% on purchases; 22.99% – 31.99% for cash advances.

Annual fee: $0

The Neo Secured Card is the best secured credit card in Canada, with no annual or monthly maintenance fees and above-average rewards.

This card does not require a hard credit check to qualify, and you can provide security funds as low as $50.

Neo Secured Credit

Rewards: Earn an average of 5% real cash back on purchases.

Welcome offer: Up to 15% cashback on your first-time purchases, plus a $25 welcome bonus.

Interest rates: 19.99% – 29.99% for purchases; 22.99% – 31.99% for cash advances.

Annual fee: $0

Credit limit: Starts at $50.

Credit score required: Poor or bad credit score.

Tangerine Bank: Credit Cards

Tangerine also offers two credit cards:

The Tangerine Money-Back Credit Card is an entry-level no-annual-fee card requiring a minimum of $12,000 in annual income and a 600+ credit score.

Cardholders earn 2% cash back in two categories of spending plus one additional 2% cash back category if they deposit their rewards in a Tangerine savings account.

All other purchases with the card earn at a 0.50% rate.

Tangerine Money-Back Credit Card

Rewards: Earn up to 2% unlimited cash back in up to 3 spending categories and 0.50% on all other purchases.

Welcome offer: Get an extra 10% cash back on up to $1,000 in spending in the first 2 months ($100 value); 1.95% balance transfer rate for 6 months.

Interest rates: 19.95% for purchases, balance transfers, and cash advances.

Annual fee: $0

The Tangerine World Mastercard also has no annual fees.

It offers the same cash back rates as its entry-level counterpart, plus

- Rental car insurance

- Mobile device insurance

- Complimentary membership in Mastercard Airport Experiences Provided by Loungekey, etc.

Tangerine World Mastercard

Rewards: Earn up to 2% unlimited cash back in up to 3 spending categories and 0.50% on all other purchases; VIP perks.

Welcome offer: Get an extra 10% cash back on up to $1,000 in spending in the first 2 months ($100 value).

Interest rates: 19.95% for purchases, balance transfers, and cash advances.

Annual fee: $0

Verdict: The Neo Secured Card is a great option if you have bad credit and are trying to improve your credit score.

If you have an annual income of $60,000 or higher, you will get more benefits from the Tangerine World Mastercard.

Neo Financial vs. Tangerine: Investments

Neo Financial recently introduced Neo Invest, a robo-advisory service offered in partnership with OneVest.

You can invest as little as $1 and have a professionally-managed portfolio built using Exchange-Traded Funds (ETFs).

Your investment assets are held with CI Investment Services.

Tangerine Bank offers a variety of ways to invest, including mutual funds, ETF portfolios, and GICs. You can hold these assets inside non-registered and registered investment accounts.

Verdict: You get more options with Tangerine Bank.

Neo Financial vs. Tangerine: Borrowing

Neo Financial does not offer personal loans or lines of credit. However, you can use it for your mortgage or HELOC.

Tangerine Bank clients can access the following:

- Mortgage loans

- Line of credit

- HELOC

Verdict: Tangerine = Neo Financial.

Other Factors To Consider

Convenience

Neo Financial and Tangerine are online financial institutions. There is no branch location you can walk into.

For customer service, you can reach an agent via phone or email.

Tangerine clients can use Scotiabank ABMs for free, which can be more convenient if you routinely conduct transactions at an ABM.

Verdict: Tangerine = Neo Financial.

Fees

Some service fees apply with both Neo and Tangerine.

For Tangerine:

- Canadian drafts: $10

- Inactivity fee (after 1 year): $10

- Overdraft protection: $5

- NSF fee: $45

- Paper statement: $2

- ABM withdrawal in Canada (non-Scotiabank): $1.50

- ATM withdrawal abroad (not part of Global ATM Alliance): $3

For Neo Financial:

If you subscribe to Neo Financial’s Plus or Ultra rewards tiers, you pay $2.99 or $8.99 per month, respectively.

- Foreign currency conversion fee: 2.50%

- Supplementary paper statement: $2.50

- Secondary authorized user: $10

- Rush replacement card: $29

Promotions

When you apply for a Neo Card here (Neo Secured Credit Card or Neo Mastercard), you receive a $25 cash bonus after your application is approved (limited-time offer).

For the Tangerine credit cards, you get a bonus of 10% cash back on up to $1,000 spent in the first 2 months ($100 value).

Security

Both Neo Financial and Tangerine are legitimate financial institutions.

Your deposits at Neo and Tangerine are eligible for CDIC deposit protection for up to $100,000 per category per depositor.

You should note that your deposits in the Neo Money account and Concentra Bank are combined when considering the CDIC deposit insurance.

Pros and Cons of Neo Financial

Pros:

- High interest rates on savings

- Competitive cash back rewards for credit cards

- Innovative secured credit card

- Multiple financial products

Cons:

- No in-person branch support

Pros and Cons of Tangerine

Pros:

- No-fee chequing account

- Free access to thousands of ABMs

- Competitive cash back rewards on credit cards

- Multiple financial products

Cons:

- No in-person branch support

- Low standard interest rate on savings

Neo vs. Tangerine: Summary

Tangerine and Neo Financial are good choices if you want to save on banking fees, earn more on your savings, and get a no-annual-fee credit card.

Neo HISA pays a higher interest rate and is better for savings. You could also opt for the EQ Bank Personal Account and earn high rates on general, RSP, and TFSA savings.

For a free and versatile online chequing account, the Tangerine Chequing account is one of the best.

The Tangerine credit cards are also top-rated in the cash back division.

Related:

Hi Enoch,

Hope all is well with you and your family?

I love reading your emails and product reviews.

The most recent one talks about Tangerine World Mastercard which I have.

Is Airport lounge access free with this card and if so how to gain access to an airport lounge?

Thanks,

Manish

In the “Related” links for this page (Neo vs Tangerine) the Tangerine vs EQ Bank takes you to KOHO vs Tangerine, and the EQ Bank vs Simplii takes you to KOHO vs Simplii, which led me to ask the internet the question “is EQ bank the same as KOHO” which apparently it is not. It’s a shame these links aren’t right as I really wanted to compare EQ Bank..

@Alex: Thanks for catching that. The links have been updated, so you can access the Tangerine vs EQ Bank and EQ Bank vs Simplii comparisons.