If you are shopping around for mortgage rates, It’s good to know what to expect (or not expect) from dealing with mortgage brokers or going directly to the big banks.

Before buying our first home, I didn’t understand the differences between mortgage brokers and banks. I just assumed they were all one and the same.

However, after we decided it was time to start hunting for our first home, I started researching mortgage brokers, mortgage rates, mortgage pre-approvals, and much more.

Canadians are in love with their big banks. A Mortgage Professionals Canada survey showed that only 36% of future home buyers intended to consult a mortgage broker, while 66% of respondents would consult a bank.

For clarity, I define mortgage brokers as intermediaries or middlemen between lenders and prospective home buyers (i.e. borrowers).

They shop for the best rates, negotiate on your behalf, sort out the paperwork, and get paid a commission for their services from the lending institution after the deal is completed.

Most jurisdictions in Canada require mortgage brokers to be licensed, and accredited members of Mortgage Professionals Canada are required to complete Continuing Education Units each year to maintain their designation.

Banks have loan officers who interface with clients to provide mortgage services directly. Loan officers work with clients to choose a mortgage product offered in-house by the bank.

Mortgage Broker vs. Bank (Pros and Cons)

When you seek a mortgage loan, should you go directly to a big bank or use a mortgage broker to find the best deals possible?

What factors should you be considering – Mortgage rates? Mortgage terms and conditions? Services offered?

Pros of using a Mortgage Broker

1. Free Personalized Service: A mortgage broker will not charge you a fee for shopping around for the most competitive rates. They are paid a finder’s fee by lenders. You can expect them to assist you with completing your application, advising on what documentation is needed, what the next steps are, etc.

With the growing popularity of online mortgage brokers, you can do all of your communication by email and phone calls. Mortgage brokers are incentivized to keep you happy and will try to make the process as pain-free as possible.

2. Save Time and Effort: Who has the time to research, negotiate with or contact 30 different lenders while shopping for competitive rates?

Well, mortgage brokers! They can access many lenders, including major banks, private lenders, and other financial institutions. Unlike the loan officer at the big bank, they are not “married” to any one lender.

3. Experience: Mortgage brokers have vast knowledge, tools, and lending options that they use to secure lower-rate mortgages. For those with a poor credit history or low income, a mortgage broker may be the only recourse to getting a mortgage loan.

4. Click of a Mouse: With the advent of online rate comparison sites like IntelliMortgage and Ratehub, you can compare rates from different lenders before choosing one to work with.

Cons of Using a Mortgage Broker

1. Commission Disincentive: Since lenders pay brokers commission fees after closing a deal, there is a potential conflict of interest. For example, if a lender pays more based on volume or other terms, a broker may recommend them more often and not exhaust the entire universe of lending options available.

This is only an issue if the lender recommended doesn’t have the best rate for your circumstances. To avoid this problem, use more than one mortgage broker and compare their offers.

2. Terms and Conditions: Apart from rates, mortgages also come with terms and conditions such as prepayment terms, porting rules, payment deferral options, penalty clauses, etc. While the mortgage broker is expected to highlight these differences and explain them, you can’t bank on them.

The lowest rate may come with unfavourable conditions that make them more expensive in the long run. For instance, prepayment or lump-sum payments may be severely limited. This means you cannot afford to stay on the sidelines and take whatever is offered. You should ask questions.

3. Access to non-broker Lenders: Some big banks run their own show with in-house staff (mortgage specialists or advisors). If they are not paying mortgage brokers a commission or “finders’ fee,” they have no incentive to check with these lenders or to recommend them. This essentially reduces the pool of lenders being consulted for the best rates.

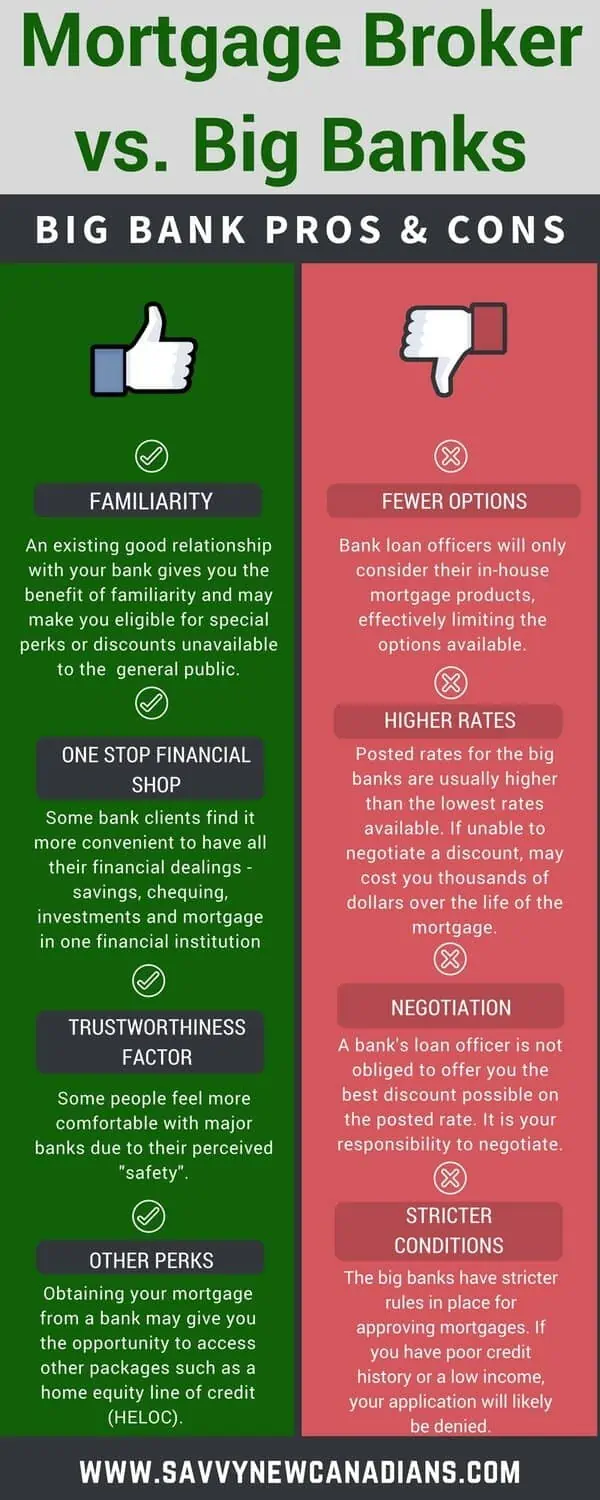

Pros of working directly with a Big Bank

1. Familiarity: If you have a good relationship with a bank, you get familiar with bank staff and their processes and may be offered special perks and competitive rates for being a loyal customer. As a longstanding client, you may have some negotiating power.

2. Other Perks: Obtaining your mortgage direct from a bank opens other opportunities and perks that may not be available when negotiating through a mortgage broker. These include access to a home equity line of credit (HELOC), and the bank may pay for a home appraisal, etc.

3. Trustworthiness Factor: Some people feel more comfortable with the “brick and mortar” feel of a bank. Major banks are perceived as “safe” and more accountable for their actions.

4. One-Stop Financial Shop: This is the convenience factor. It can be more convenient to have all your financial dealings – savings, chequing, investments, and mortgages with the same financial institution. For this reason, some will instead go directly to their bank to obtain a mortgage.

Cons of the Big Bank

1. Usually Higher Rates: Rates posted by the major banks are usually higher than the lowest rate available. If you cannot negotiate a discount, you may be paying a lot more in interest fees (think several thousand dollars extra) over the life of your mortgage.

2. Fewer Options: A bank loan officer will only consider their in-house products when offering you a rate. You lose out on the ability to compare rates across different lenders.

3. Negotiation: The bank loan officer is not obliged to offer you the best discount on their posted rate. You have to work for it. They get paid commissions on their sales, and the onus is on you to negotiate the best deal you can get.

4. Stricter Conditions for Approval: The big banks have stricter rules in place (for good reason) for approving mortgages. A mortgage shopper with a poor credit history or low income may have better success working with a mortgage broker.

A Word About Credit Unions

Most mortgage shoppers forget about credit unions when shopping for a competitive mortgage rate. However, credit unions often beat the banks regarding posted rates and should not be overlooked.

Some credit unions also offer their members extra benefits, including profit-sharing.

Conclusion

Shop around! When we were mortgage shopping, we started with the big banks, moved on to online mortgage brokers, and ended up with a credit union.

When you get a good rate, do your homework and check the fine print and penalty clauses. If you decide to go with a mortgage broker, make sure you check online rate comparison sites for a general idea of the latest competitive rates.

Featured Mortgage Offer

Neo Mortgage

On Neo Financial’s website

- Compare mortgage rates across several lenders

- Access to competitive rates and online applications.

- Available Canada-wide

- Accepts a wide range of credit scores

Related Posts:

- Best Mortgage Rates in Canada

- How To Pay Off Your Mortgage 5 Years Early

- Homewise Mortgage Review

- Mortgage Rules You Should Know

- Best Life Insurance Companies in Canada

- Is Life Insurance Worth It?

Excellent information, truly helpful. thank you for sharing